Every man a VC: On public deep-tech startups

The life of a venture capitalist is a hard one: the vast majority of their investments are doomed to fail, making them easy targets for criticism (you put how much money into Juicero?). And yet, a portfolio company will occasionally become a massive success, perhaps indicating a degree of foresight or talent on the investor’s part (assuaging their ego). The hits are big and the misses are obvious. This is all a by-product of the venture capital model (AKA the power law), which dictates that a small portion of a fund’s investments will drive total portfolio returns.

Put this way, venture investing doesn’t seem too far off from gambling – occasional dopamine creating events separated by long stretches of failure. That sounds like a pretty good gig to me! It’s like scratching lotto tickets with other people’s money. Certainly it’s more exciting than putting fractions of paychecks into an index fund for the next thirty-some odd years. The increasing prevalence of sports betting, prediction markets, and zero-day options trading suggests the average American shares my perspective.

However, most of us can’t behave like a VC, and not simply because of a lack of capital. Getting access to these early-stage investments has historically been restricted to VCs, their limited partners, and high-net-worth angel investors. Us common folk are legally barred from participating in such deals due to SEC regulations. While I think it my God-given right to lose my savings in a half-baked scam, the government disagrees. Moreover, the best deals are hard to get into; VCs often compete for allocation by offering additional value-adds besides pure capital.

Things are changing though. Take for example this year’s cohort of giant tech IPOs: it’s possible for retail investors to get economic exposure to Anthropic and OpenAI via special purpose vehicles, crypto-based perpetual futures, and plain old ownership of the already public tech companies which have stakes in the AI labs.1 SpaceX’s IPO performance was quite well-mirrored by these crypto instruments.2 Alternatively, us plebians can just buy normal stock once it’s available. These companies are after all deeply unprofitable and will ostensibly grow! That’s all well and good, but it’s still hard to paint a picture of 10- or 100x-ing your investment when you’re getting in at a $1-2 trillion valuation. If only I, a relatively cash-poor retail investor, could get in on high-risk companies before they reach valuations in the hundreds of billions.

Thankfully, a new class of investments is rising to fill this underserved need. I call them the ‘public deep-tech startups,’ and they are defined by a combination of enormous technical risk, voracious capital needs, and often, religious retail fervor. To the untrained eye, these firms look like they’d be best funded by some combination of federal dollars and venture capital, given their dual technical and commercial risks. To the sophisticate however, these companies are clear fits for public markets.

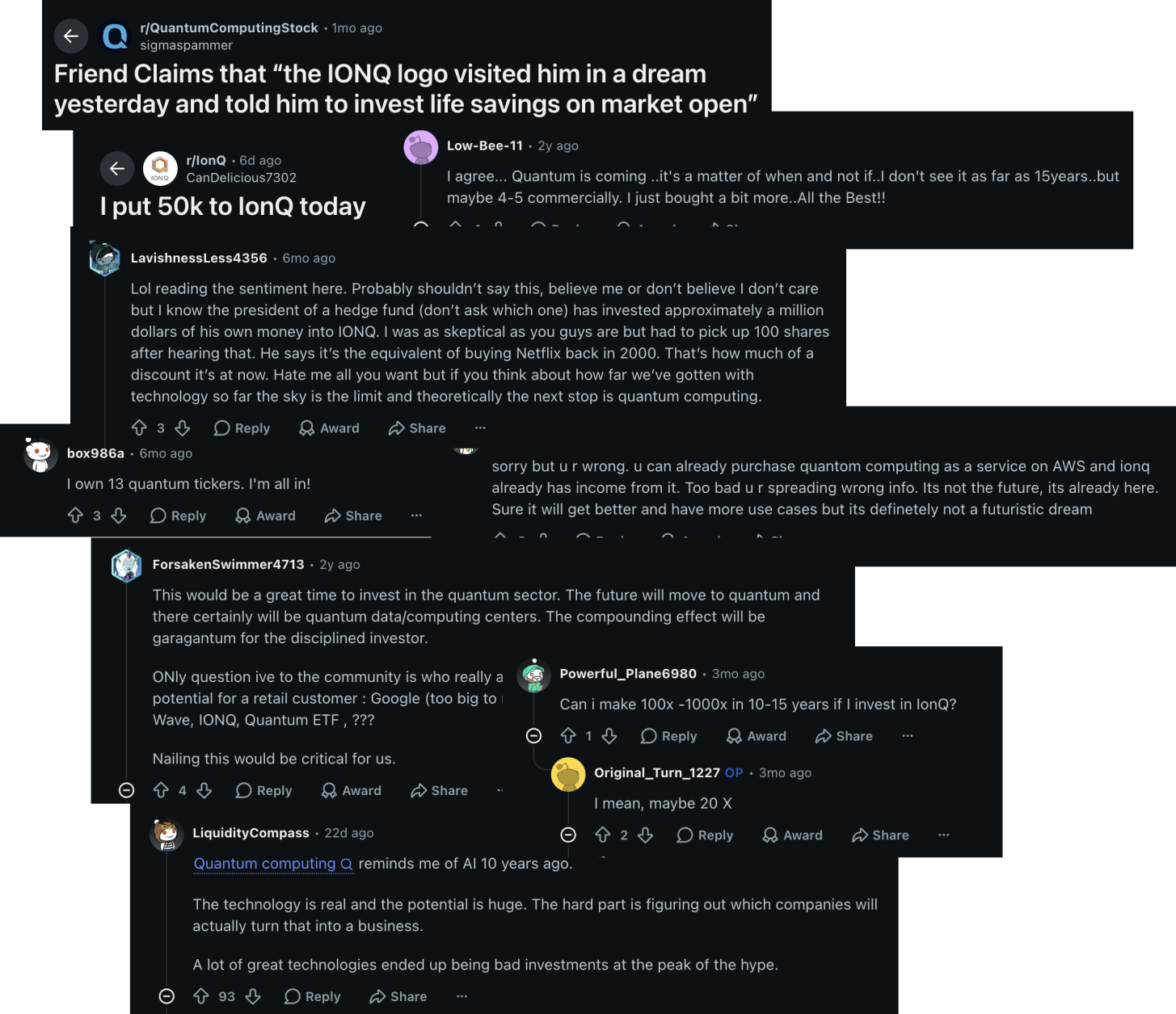

The prototypical example is IonQ, Inc. This is a $10-30 billion dollar public company that specializes in the development of trapped ion quantum computers. Quantum computing is a very confusing, famously opaque field, and I’m not going to explain it in detail now. For the purposes of this piece, please take these points as a given: 1) Neither IonQ nor any of its competitors have a scaled, functioning quantum computer today; 2) It will take many more billions of dollars of investment to build such a device, and there is no guarantee that any individual company’s technical approach will succeed; 3) useful commercial applications (and thus value) for this quantum computer are sparse and uncertain. If you’d like to learn more about these points, or about the quantum computing space in general – I’ve written a book about the topic that I plan to release soon. This piece is in fact covert advertising for said book; please comment enthusiastically if you are interested!

OK – given those postulates, I hope you can buy that IonQ is primarily a speculative investment. It entered the public markets during the SPAC3 boom of 2021, joined by its quantum computing peers Rigetti and D-Wave. The trio has bucked the traditional SPAC narrative (poor returns, varying degrees of fraud, etc.) and done fairly well over the past 5 years, buoyed by enormous retail interest in the sector, albeit marred by significant volatility. These companies have used their public status to their advantage: they’ve sold equity, sold warrants, and used their stock to conduct aggressive acquisition strategies.

And now a new wave of public deep-tech companies is emerging, perhaps influenced by the success of this vanguard. In the quantum space, we’ve seen Infleqtion, Horizon Quantum, Xanadu, IQM, and Quantinuum go public in the past six months, with several more peers on the way (Pasqal, Terra Quantum, SeeQC). Fusion energy companies General Fusion and TAE Technologies are planning to go public (GF via SPAC, and TAE via merger with, oddly enough, the Trump Media & Technologies Group), and Avalanche Energy is reportedly exploring an IPO.4 The fission industry isn’t to be excluded either! In addition to NuScale and Oklo, two small modular reactor companies which executed their SPACs in 2022 and 2024 respectively, Deep Fission, a startup with the goal of putting fission plants a mile underground (an idea which has garnered significant skepticism5), went public late last year. Each of these companies has huge amounts of technical risk remaining before they can even attempt to bring a product to market. This is uncharacteristic of a typical public company, which usually is at least mature enough to have something to sell.

It’s worth noting that in most of these cases, the stock’s value is disconnected from business fundamentals. I don’t mean to rag on IonQ, but their numbers are pretty representative: Valuation of ~$20 billion, 2025 revenue of $130 million, and total earnings of negative $186 million (with several billion in cash sitting on their balance sheet). To have the numbers make sense (god help you if you want to build a DCF model), there has to be some incredible growth in both revenue and profitability.

These companies are willing to make rather extreme and perhaps not well-founded claims about technical capabilities, roadmaps, and commercial traction.6 The quantum companies have historically lagged behind their projections of qubit counts and trotted out half-baked industry partnerships that haven’t quite led to real-world adoption. Falling behind timelines is so common in the fusion industry that everyone knows the joke about it always being ten years away (to be fair, this is true of the industry as a whole, not just these public firms – deep-tech is hard!).

Quick digression: There’s actually an industry where this sort of behavior is somewhat normal – biotech! Since the successful IPO of Genentech all the way back in 1981, early-stage, pre-product biotech companies have been going public (with wildly varying results). To some extent, these IPOs look a lot like the ones I’m discussing – retail investors went wild over Genentech and its ilk!7 But the biotech industry is a bit different, especially now. First, the companies going public are generally more proven: they often have drugs in clinical trials, and there’s a robust niche of pre-IPO institutional investors who help set valuations.8 Second, there are opportunities for these companies to exit without going to the public markets, given the existence of an active pharmaceutical M&A market. There’s no parallel for a quantum computing or fusion company. Finally, the scale is different. Quantinuum just raised $1.7 billion on a roughly $15 billion valuation in its IPO; that’s 2.5x larger than the largest biotech IPO ever! So I’d argue there’s something unique going on here, but it clearly inherits some characteristics from biotech financing.

One has to wonder if this is a case of adverse selection. Private markets have demonstrated a willingness to fund large, late-stage rounds for some of these companies’ competitors, including $465 million for Helion, $860 million for Commonwealth Fusion, $300 million for Atom Computing, and $1 billion for PsiQuantum. Are public markets just getting access to companies that institutional investors have passed on? Is it ‘wrong’ for these companies to be publicly traded?

I can’t answer these questions, but I’m not sure they even matter. I’ve spent the better part of a year trying to understand the quantum computing industry, and I would be hard put to decide which hardware modality, let alone which company, will be most successful in the future. Institutional investors are just as unsure too! I don’t mean to talk down the expertise of the average retail investor, but I can see their Reddit posts, and they aren’t exactly domain experts. My impression is that the average retail deep-tech enthusiast is operating primarily off of vibes, buying lotto tickets for the broad industry. Why they might choose to invest in IonQ rather than Quantinuum; Oklo over Deep Fission; quantum instead of fusion -- is totally beyond me. Even if they had their pick of the litter – access to public and private companies – maybe they’d still pick the ones that are public today! What they are looking for is exposure to deeply asymmetric, high-risk technological bets, with a philosophy not totally unlike a VC looking to put money into these sectors. Each of these companies is still relatively small, and it isn’t insane to convince yourself that your investment might appreciate by an order of magnitude, especially considering how volatile these valuations are.

What I’m trying to say is that while I’m deeply skeptical of a hard-tech startup that chooses to go public before it has revenue or product, I don’t think this is a simple narrative of exploitation of retail investors. These companies have correctly identified a need underserved by the public markets: the desire to be one’s own VC. Is this misguided? Probably. But if we live in a world where it’s easy to throw money away on sports bets and prediction markets, retail investment going to deep-tech R&D doesn’t sound half as bad.

See the inimitable Matt Levine on this: https://www.bloomberg.com/opinion/newsletters/2026-06-04/get-your-spacex-bets-in-now

https://www.wsj.com/livecoverage/spacex-ipo-stock-market-06-12-2026/card/pre-ipo-futures-anticipate-30-pop-in-spacex-s-stock-i4LgYSnnY4N0hIBZSFM0

A ‘special purpose acquisition company’: A public entity is formed, raises money, then goes and merges with an existing private entity. This alternative way of going public bypasses the traditional IPO process with lighter regulatory hurdles, specifically allowing the private company to make forward-looking claims.

https://www.axios.com/pro/climate-deals/2026/05/27/avalanche-energy-jefferies-fusion-ipo

https://heatmap.news/energy/deep-fission-small-reactors

For example, IonQ will reportedly jump two orders of magnitude in qubit count, from ~100 to 10,000, in a year: http://archive.today/toYcC

https://www.upi.com/Archives/1980/10/18/Genentech-brings-big-bucks-in-Wall-Street-debut/8435340689600/

https://pmc.ncbi.nlm.nih.gov/articles/PMC8953971/

Interested in your take on established companies that have recently hard pivoted to quantum (e.g. IBM w/ Anderon) … as well as that book!